Farm Bureau Insurance: A Comprehensive Guide

Farm Bureau Insurance is a well-established insurance company that has been providing a wide range of insurance products and services to its members for many years. With a strong focus on serving the needs of farmers, ranchers, and rural communities, Farm Bureau Insurance has built a reputation for its commitment to customer service, financial stability, and community involvement. In this comprehensive guide, we will delve into the history, products, services, and overall value proposition of Farm Bureau Insurance, exploring its strengths and weaknesses to provide a thorough understanding of what it offers to its members.

History and Background

![]()

Farm Bureau Insurance traces its roots back to the early 20th century when farmers and ranchers recognized the need for a collective voice to address their unique challenges and advocate for their interests. The Farm Bureau, a grassroots organization representing agricultural interests, was formed to provide a platform for farmers to come together, share knowledge, and work towards common goals.

As the Farm Bureau grew in influence and membership, it became evident that farmers also needed access to affordable and reliable insurance coverage. Traditional insurance companies were often hesitant to serve the agricultural community due to the perceived risks associated with farming and ranching. In response to this need, Farm Bureau organizations in various states began to establish their own insurance companies to provide tailored coverage to their members.

Over time, these state-level Farm Bureau Insurance companies evolved and expanded their product offerings to include a wide range of personal and commercial insurance solutions. Today, Farm Bureau Insurance operates in multiple states, providing coverage to individuals, families, and businesses across rural and urban areas.

Products and Services

Farm Bureau Insurance offers a comprehensive suite of insurance products and services designed to meet the diverse needs of its members. These include:

-

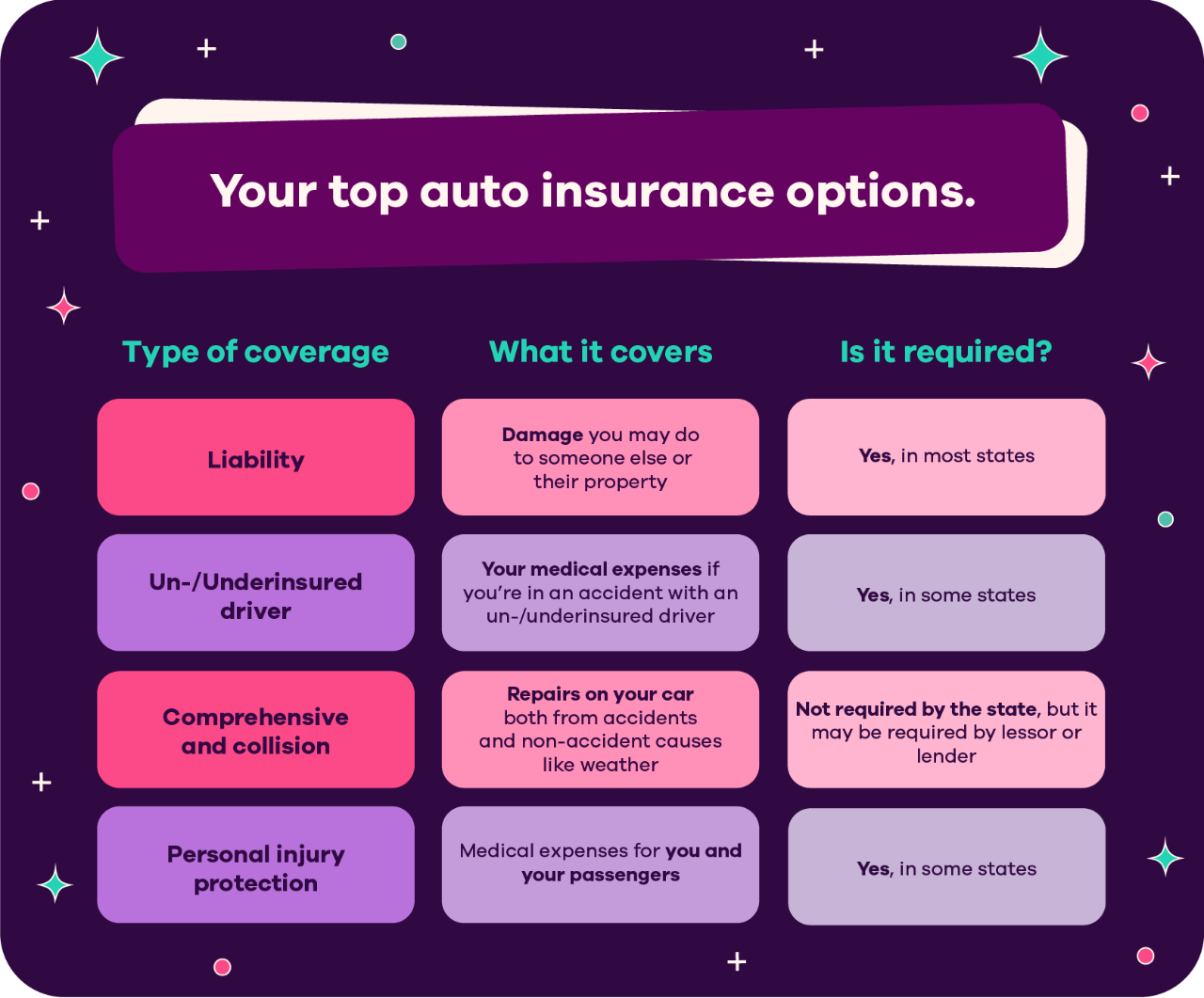

Auto Insurance: Farm Bureau Insurance provides auto insurance coverage for a variety of vehicles, including cars, trucks, motorcycles, and recreational vehicles. Their auto insurance policies typically include coverage for liability, collision, comprehensive, uninsured/underinsured motorist, and medical payments.

-

Home Insurance: Farm Bureau Insurance offers homeowners insurance policies that protect homeowners against financial losses resulting from damage to their homes and personal property. Their homeowners insurance policies typically include coverage for fire, wind, hail, theft, vandalism, and liability.

-

Farm and Ranch Insurance: Farm Bureau Insurance specializes in providing insurance coverage for farms and ranches. Their farm and ranch insurance policies typically include coverage for farm buildings, equipment, livestock, crops, and liability.

-

Life Insurance: Farm Bureau Insurance offers a variety of life insurance products, including term life insurance, whole life insurance, and universal life insurance. Their life insurance policies provide financial protection to beneficiaries in the event of the insured’s death.

-

Health Insurance: Farm Bureau Insurance offers health insurance coverage through partnerships with leading health insurance providers. Their health insurance options include individual and family health plans, as well as Medicare supplement plans.

-

Business Insurance: Farm Bureau Insurance provides business insurance coverage for a variety of businesses, including small businesses, farms, and ranches. Their business insurance policies typically include coverage for property damage, liability, workers’ compensation, and business interruption.

Benefits of Choosing Farm Bureau Insurance

There are several benefits to choosing Farm Bureau Insurance as your insurance provider:

-

Local Expertise: Farm Bureau Insurance agents are typically local residents who understand the unique needs of their communities. They can provide personalized advice and guidance to help you choose the right insurance coverage for your specific situation.

-

Competitive Rates: Farm Bureau Insurance offers competitive rates on its insurance products. They also offer a variety of discounts to help you save money on your insurance premiums.

-

Excellent Customer Service: Farm Bureau Insurance is known for its excellent customer service. Their agents are responsive and helpful, and they are committed to providing you with the best possible insurance experience.

-

Financial Stability: Farm Bureau Insurance is a financially stable company. They have a strong track record of paying claims promptly and fairly.

-

Community Involvement: Farm Bureau Insurance is committed to supporting the communities it serves. They sponsor a variety of local events and organizations.

Drawbacks of Choosing Farm Bureau Insurance

There are also some potential drawbacks to choosing Farm Bureau Insurance:

-

Limited Availability: Farm Bureau Insurance is not available in all states.

-

Membership Requirement: In some states, you may need to be a member of the Farm Bureau to purchase insurance from Farm Bureau Insurance.

-

Limited Online Tools: Farm Bureau Insurance’s online tools are not as comprehensive as those offered by some of the larger national insurance companies.

Overall Value Proposition

Farm Bureau Insurance offers a compelling value proposition for individuals, families, and businesses seeking comprehensive insurance coverage and personalized service. With its strong roots in the agricultural community, Farm Bureau Insurance understands the unique needs of farmers, ranchers, and rural residents. Their local agents provide expert advice and guidance, helping members choose the right insurance coverage to protect their assets and livelihoods.

Farm Bureau Insurance’s commitment to customer service, financial stability, and community involvement sets it apart from many other insurance companies. While its availability may be limited in some areas and its online tools may not be as advanced as those of its competitors, Farm Bureau Insurance remains a solid choice for those seeking a trusted insurance provider with a strong focus on local expertise and community support.

Conclusion

Farm Bureau Insurance is a well-established insurance company with a long history of serving the needs of farmers, ranchers, and rural communities. With a comprehensive range of insurance products and services, a commitment to customer service, and a strong focus on community involvement, Farm Bureau Insurance offers a compelling value proposition for those seeking reliable insurance coverage and personalized support. While its availability may be limited in some areas and its online tools may not be as advanced as those of its competitors, Farm Bureau Insurance remains a solid choice for those seeking a trusted insurance provider with a strong local presence.